In 2017, Janet Yellen, the then Chair of the Federal Reserve Bank of America, which is arguably the most prominent and influential financial position to be held by anyone throughout history, boldly stated that “another financial crisis not likely in our lifetime”. In every sense, Yellen must be considered the highest source of authority for a statement of such extreme confidence to originate from.

However, historically speaking, Yellen isn’t alone in taking such optimistic and arguably audacious prognostications. In fact, even some of the most notable names in the history of economic thought have ventured this far, “On 16th October 1929 Yale University economics professor Irving Fisher declared that the US stock prices had ‘reached what looks like a permanently high plateau“. The problem for Professor Irving Fisher was that despite his well-recognized expertise and authority on such matters, it was only “Eight days later, on ‘Black Thursday’, the Dow Jones Industrial Average declined by 2%. This is when the Wall Street crash is conventionally said to have begun“1. To defend this initial position, Fisher stated “It was the psychology of panic. It was mob psychology, and it was not, primarily, that the price level of the market was unsoundly high … the fall in the market was very largely due to the psychology by which it went down because it went down.”3.

If this defense is either true or even for that matter held as true by Fisher, the question arises, why on earth should anyone attempt to predict the stock market or the future of the economy in the first place? That is to say if the market is subject to such irrational chaos at the ‘whim’ of a mob, wouldn’t all predictions carry as much weight as any other prediction, regardless of whether that source is a coin toss or an internationally recognised economist, or for that matter the head of the most powerful financial institution that the world has ever seen? The problem, however, with Fishers’ defense isn’t that the market wasn’t subject to mob psychology throughout 1929 or throughout the decade that followed 1929, but rather the problem with Fishers’ position was that the market would be anything but mob psychology at any point in time or to infer that mob psychology is in any way irrational in light of market forces.

“October. This is one of the peculiarly dangerous months to speculate in stocks. The others are July, January, September, April, November, May, March, June, December, August, and February.”

—Mark Twain, Pudd’nhead Wilson

In 1998 Hugo Chavez was elected president of Venezuela, and in 2003 the country experienced a huge positive exogenous windfall as oil prices started to climb. The rising price of oil on the small nation could best be described as a rare ‘gift from heaven’. The oil-rich country under the leadership of Chavez nationalised the nation’s oil exports and radically expanded the role of the government with the ultimate result being that private industry was “forced out” as Chavez famously “claimed” businesses and placed them in the state’s hands. Government employment grew dramatically during this time and Chavez grew popular through huge social welfare and healthcare initiatives. For a while, Politicians, Actors and Nobel prize-winning Economists alike praised Venezuela’s President Hugo Chavez for his ‘progressive’ socialist policies and nation’s wealth created by their oil guzzling northern neighbors. Chavez’s attention to the poor, his dedication to healthcare and education meant that the ‘mob’ loved Chavez, and in a sense, they would have been irrational not to. Chavez was “proof” that the centrally planned socialist economy could work despite the fact that even while the nation’s wealth was increasing, budget deficits grew. Following the collapse in the price of oil and the subsequent and arguably inevitable collapse of the country who built its entire economy around this one export, the mob that once loved and treasured Chavez turned from loving their government to rioting against it. One interviewee describes the situation in Venezuela as she “believed the country hit rock bottom when she ‘saw people trawling through dumpsters to find pizza crusts and fruit peelings, which they ate immediately, only to see the following day lineups to these dumpsters and stores selling the privilege to trawl them’”.

The problem of Venezuela isn’t that the Venezuelan people were illogical to like and support Chavez, just the same as the once-prosperous Venezuelans who were now starving, weren’t illogical to dumpster dive. The problem with the mob wasn’t lack of logic, it is that the logic was short-sighted. Mob psychology ultimately drove Venezuela to its socialist ascent as it drove it to its disastrous collapse and in this sense, factors that led to the collapse of Venezuela, can also be seen to be contributing factors in the major western economic collapse including the Great Depression of 1929, the dot-com bubble of 2001 and the GFC of 2008, which is that: mob psychology rules economies on the way up and on the way down, that these mobs are smart but only in getting the food from their hands to their mouths, and while the potluck is good, few complain.

The mob is not irrational but its collective logic has at least even greater limitations to that of the individuals within the mob simply because, to unify a collective of people with different hopes, dreams and beliefs, around a single creed, must mean that that creed is simplified and free of nuance. To mobilise a lot of people, you first have to dumb down the message. This mob, which was comprised in part of a collective desire for group prosperity and in a much greater part, a convergent zeitgeist of individual prominence through economic means, means that the mob, time and time again fails to achieve either of these goals at an aggregate level; that is at least without major hiccups. And this failure isn’t because the mob is illogical, but because it’s only good at the short game; the mob can only see so far forward and only so far back. Regardless of how much better off the mob may be from that of only a few decades ago, the desire and impulse of the mob will be to still believe that the current system is deeply flawed and oppressive, that is unless significant and monumental growth is being experienced by the vast majority of the mob at that immediate point in time. The only growth and prosperity that will truly pacify the mob, is usually that of massive, unstable and unsustainable growth.

It’s hardly an insightful observation to notice that mobs are logical but myopic. Arguably, the fundamental problem with all people isn’t that we’re hedonists, but that we are, for the large portion of the time, myopic hedonists. If of course, myopic hedonism is the fundamental issue with humanity, we should see this theme of in just about every major world religion that tries to deal with the fundamental malaise of existence, and I think we do. For example, the God of Christianity wasn’t calling his followers to be stoics, the claim wasn’t that the Christian should live a completely ‘unsatisfying’ and altruistic life and somehow find some deeper fulfillment through it, but rather that the Christian should live as the Christ lived, which was according to the writer of the new testament book Hebrews: “For the joy set before him he (the Christ) endured the cross, scorning its shame, and sat down at the right hand of the throne of God.”4, which, in part, and in a crude manner means something to the effect that: living for others can be for self-motivated reasons.

According to the writer of Hebrews, the Christ of Orthodox Christianity suffered the death on the cross because of the better things to come, namely “the joy set out before him“; and the Christian is promised a similar reward for the same motive. So important is this reward, this ‘long-term goal’, that Saul of Tarsus who became Paul, writes in his first letter to the Corinthians in chapter 15 that, without the reward first gained by the Christ, that the whole faith is pointless and “if (the) Christ has not been raised, (Paul’s) preaching is useless and so is ‘the Christian’s faith” and, he states it again in verse 17 “if Christ has not been raised, ‘the Christians’ faith is futile“, and then again in verse 19 “If only for this life we have hope in Christ, we are of all people most to be pitied“5.

Obviously, Paul did not write these statements as a rich 21st century Western Christian who listens to sermons in airconditioned comfort each week, but rather by a man who gave up everything to follow this Christ and then suffered immensely for it. C.S. Lewis the late Christian apologist makes a similar observation in regards to the myopic nature of man, where he states “It would seem that Our Lord (the Christian God) finds our desires not too strong, but too weak. We are half-hearted creatures, fooling about with drink and sex and ambition when infinite joy is offered us, like an ignorant child who wants to go on making mud pies in a slum because he cannot imagine what is meant by the offer of a holiday at the sea. We are far too easily pleased.” However, it’s not just in Christianity that we see this nucleus theme of myopic hedonism playing out, rather, core to the moral worldview of just about every major world religion that I’m somewhat familiar with, is this theme of ‘delayed pleasure for long-term gain‘, with the flaw in humans being that humans, individually and acting as a mob, want to always shortcut to the reward. In fact, the key difference between children and adults as far as decision-making capacity is concerned, is that children aren’t able to make the same long-term weighted choices that adults do; nonetheless, it is common for adults to revert to childish myopia as time and time again we willingly ignore the long-term consequences and rewards for our actions. Why do we lie? Because telling the unembellished truth often leads to short-term pain and after the short-term pain, only then is the long-term reward a possibility. Why do we steal? Because we want the product of another’s labor without the sacrifice or suffering that is required to make or earn that product. Why do we fornicate? Because building a trusting and fulfilling marriage is hard and adultery is easy. Why do we bet on stocks?… okay.. there are many reasons why we might be playing the market and I’m not really making a moral case for whether or not the equity market is fundamentally wrong or right, but in general, the mob plays the market to make short-term gains, that is to earn wealth that they haven’t worked for, to ultimately, get rich quick or at the very least, to not miss out on an opportunity to get rich quick. In fact, I would argue that in every way the modern market is the very definition of mob rule, the market is the collective of human nature and the epitome of its greatest malady, myopic hedonism. When the market goes up, it’s because the mob thinks it will continue to go up, and when it goes down, it is because the market is simply concerned with minimizing losses. But, what the stock market can’t dictate through myopic euphoria is the fundamentals that drive the euphoria. The market is not reality but is tied to reality – through a damn choke leash.

The Vengeful Fundamentals

In the aftermath of the Global Financial Crisis of 2008, much blame was levied at the banks, mortgage institutions and huge investment banks who managed to exploit society’s most vulnerable with the idea that owning a home or even multiple homes, was well within the grasp of the everyday American regardless of whether or not that American even had a job and regardless as to whether or not it was mathematically feasible as to whether that individual would ever be able to repay the interest on the mortgage let alone the principle. However, despite this gross exploitation, very few individuals responsible for the chaos that ensued ever faced significant legal repercussions. Initially, looking into this matter, I believe most would blame the lack of criminal prosecutions on ‘mass corruption’ with good reason to believe that there existed a two-tier policing system, one which obviously wasn’t concerned with locking up people in places of power and wealth. And, while this may certainly be the case and without daring to defend any of the large corporations involved or the individuals who ran them, I believe that the issue is more complicated than that. Looting without major repercussions for the looters is sometimes made possible when enough people engage in the looting. The system that would usually protect private property and ensure that thieves are bought to justice can, demonstrability be overwhelmed when too many engage in the act at any one time. In a sense, the same may be the case for those who were responsible for the events leading to the GFC.

Those who purchased the sub-prime mortgages were to some degree responsible for taking out loans that they should have known that they would never be able to repay, the bankers were responsible for loaning money irresponsibly and taking advantage of those who didn’t do their due diligence, the investment banks were responsible for repacking those loans in such a way as to hide the investment’s true nature through ‘probability alchemy’, the rating agencies were responsible for… pretty much not doing their job at all for fear of losing market share to other ratings agencies who also did do their job resulting in a classic worst-case but predictable ‘nash equilibrium’. The fed was responsible for enabling the bubble to get as large as it did with long-lasting low-interest rates post the dot-com bust, the government was responsible for not imposing the correct regulations on the banking industry to protect against these observed malpractices happening, while at the same time as distorting the market through, more or less everything that they did do during the Clinton-Bush era where they introduced policies that sounded benevolent in nature but ultimately provided the landscape for the market to collapse.

In a sense, the bubble of the US housing boom, in the run-up to 2008, held many of the same characteristics as the 2001 dot-com bubble, the 1928 Florida housing bubble, the recent 2017 bitcoin bubble, and even the 1720 Mississippi stock bubble; that is that the bubble was blown up by rational people who were captivated by the possibility of exponential returns who felt as though they wouldn’t get caught out, as long as they were part of the herd, they believed that they were safe. The reality is that ‘The chance of gain is by every man more or less overvalued, and the chance of loss is by most men undervalued.’ 5.

The Mob doesn’t appear when there is market strife, it is always present, running the market up and running the market down, but at all times, the mob is out for itself. Sometimes the mob is camouflaged by prosperity, but it is always captivated by the short term possibility of making more. The mob rode the housing bubble higher and higher, afforded to it by poor Federal Reserve management, afforded to it by government and rating agency malpractice, afforded to it by greedy investment bankers, afforded to it by moronic regulations that broke that ever-important link between risk and responsibility, but ultimately the market collapsed and not because the mob was fearful of losing money, although that certainly played a part in the unveiling downward spiral. The market didn’t collapse because of any waking irrational animalistic spirit, although, it certainly did wake. The market ultimately collapsed because the fundamentals started to give way to mountains of unserviceable bad-debt in the face of increasing interest rates. In short, the 2008 housing bubble collapsed because fundamentals fought back. In the end, it was the fundamentals vs the mob, and the fundamentals always win. The fundamentals whipped the choke collar of reality, and the financial world spluttered.

What is Wealth?

When we think of wealth or more specifically a the connotations around what may be considered a ‘wealthy nation’, our minds may be inclined to think of grand mansions, sports cars, servants, holidays and fine clothes, but before we have the chance to contemplate the luxury afforded by money, we first tend to think about the exact dollar figure that facilitates the purchases. Very rarely would anyone consider an individual who is scarcely clearing the interest on their mortgage as ‘rich’, regardless of how grand their house may or may not be. No, the measure of wealth usually is measured by the sheer exposure of choice that the individual has. That is, the true measure of wealth that we associate with any individual, is measured by the relative opportunities that that individual is exposed to. These opportunities usually include choices on where they choose to live, what they can wear, what they can eat, where they can study, where they can travel, what they choose to do with their time. That is, the dollar figure attached to an estate is a measure of opportunities that the estate holder has, meaning that the measure of what is a wealthy nation, is defined by the productive capacity of that society and the degree of opportunity that an individual has relative to others in other societies. A man who would be considered rich in Uganda may be considered middle class or even poor in Australia, but because of the relative difference in opportunity between the observers in one country to the other, the connotations of what is considered “wealthy” can be considered very different between each country.

Unsurprisingly, both in geographic and historical terms, no Australian could really be considered poor except, maybe, for maybe those in the most remote areas or those especially down on their luck and on the streets. The association of wealth is relative to the exposure of the masses to those with more opportunity than them as: the association with poverty is also relative in the same manner. In most western nations, to have shelter along with running water and electricity would scarcely be considered rich. Nor would the access to some form of healthcare, education and job prospects. But, to the vast majority of the world’s population both past and present, these would be seen as luxuries. And hence, unsurprisingly money in terms of the sheer number figure, ‘nominal quantity’, isn’t important in determining one degree of wealth to another. The nominal figure attached to money means nothing, ultimately money is only as valuable as the productivity attached to that dollar. If the material, technological and intellectual assets of a society grow at a faster rate than the population growth, then the society becomes aggregately, relatively wealthier, and money is the distribution of the opportunity between consumers. Basically, the more goods and services, available to a nation, the wealthier that society becomes on an aggregate level.

At the realisation that cash isn’t the measure of wealth but the measure of the distribution of wealth within a nation, it’s easy to see how 1. There may be a disconnect between perceived aggregate wealth within a society and the actual productive capacity of that society, 2. Changes to the money supply may or may not have an impact on the productive capacity of any particular nation either over the short-run or the long-run, and 3. How easy it would be for politicians, bureaucrats, and businesses to use the nominal monetary figures to conceal or distort what may be happening at a fundamental level within the economy.

Colloquially, the differences between the “cash-based/nominal financial world” and the “productive/fundamental world” are referred to as the differences between the “nominal” and the “real”. While all reports and attention are usually focused on the nominal world, ultimately, it’s the fundamentals, the real world figures, that matters most in determining current and future wealth of a nation and while changes in the nominal world may affect both in the short and long run what happens in the real world, the nominal world can also be used to distract and obscure what’s happening in the real. That is to say, the figures that we rely on to paint us the picture of what is happening in the real, maybe equally used to conceal to paint us a very different one.

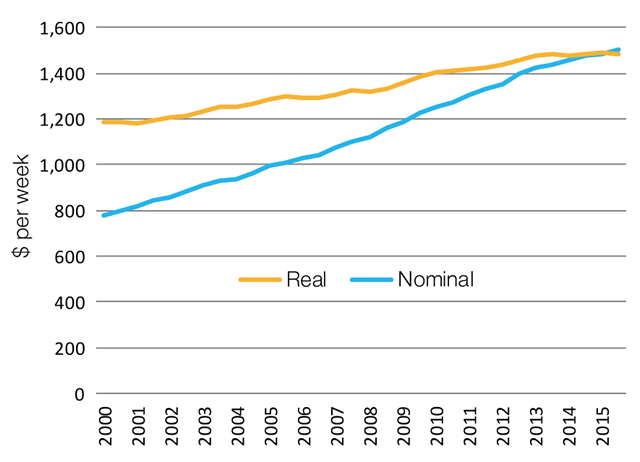

At a household level, the rate of real wage growth has been growing at a slower rate to nominal wage growth. The graph below depicting the changes in the Australian labor market.

Source: ABS, Average weekly earnings, cat. no. 6302.0, Original data. Real wages are shown in June 2015 dollars

However, the narrow definition of money at the day-to-day CPI level isn’t telling the whole story of nominal financial growth.

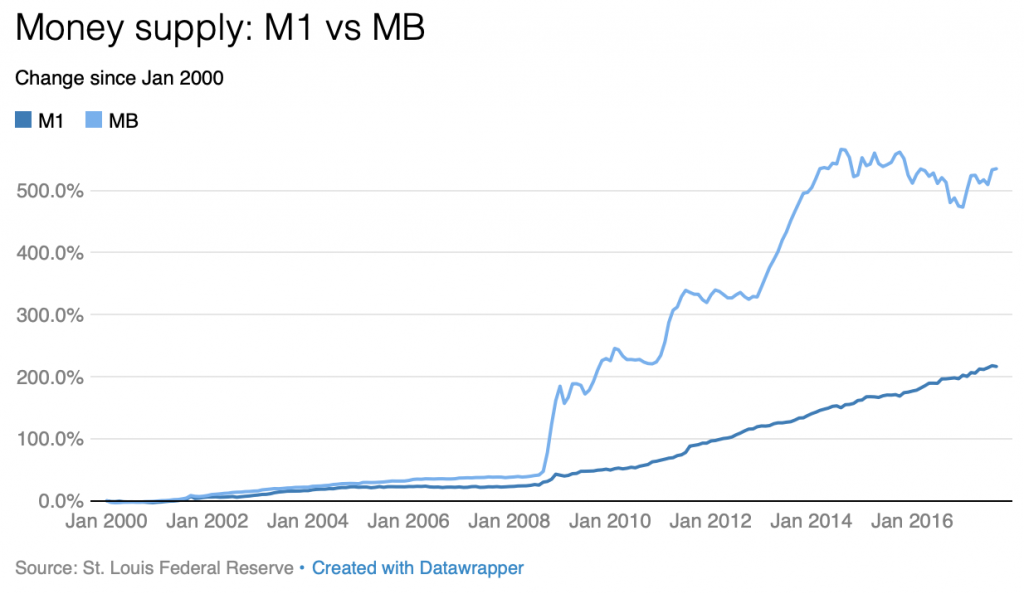

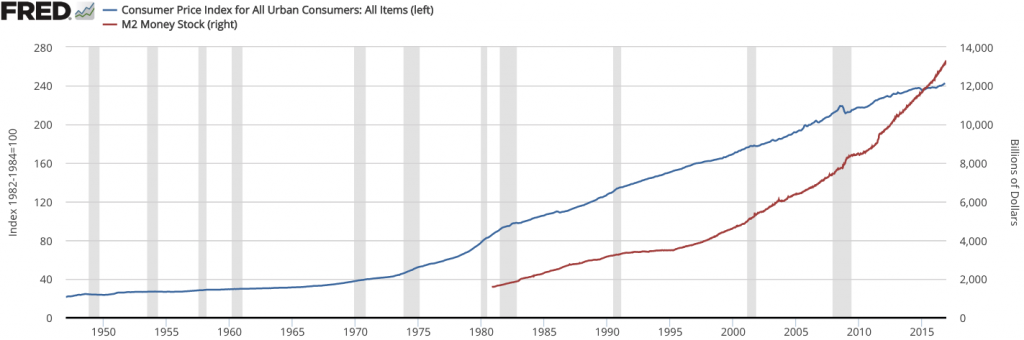

Since the GFC, the Federal Reserve Bank of America dramatically expanded its balance sheet through a process known as “Quantitative Easing” or “QE” for short. QE is ‘newspeak’ for free money. The age-old saying, “money doesn’t grow on trees”, is correct, the reality is that it’s created out of thin air by powerful people who own the central bank of the world’s reserve currency along with central banks and governments around the world. Money is somewhat counter-intuitively hard to define, but the key difference to note is the distribution of currency in the financial sector and that which is in the consumer sector.

Monetary Base, or MB for short, is a measure currency in circulation in the hands of the public or in the commercial bank deposits which include the growth of the FED’s balance sheet as opposed to M1 which is an indicator for the amount of physical currency that is in circulation and does not include bank reserves. The growth of MB through the FED QE, as opposed to the liquid money that is in circulation, can be seen in the graph below:

While there is a correlative relationship between the two measures of money, one thing can be easily observed, which is that the growth in MB has far outstripped M1 for over a decade, which is only possible if there has been little to no real economic growth.

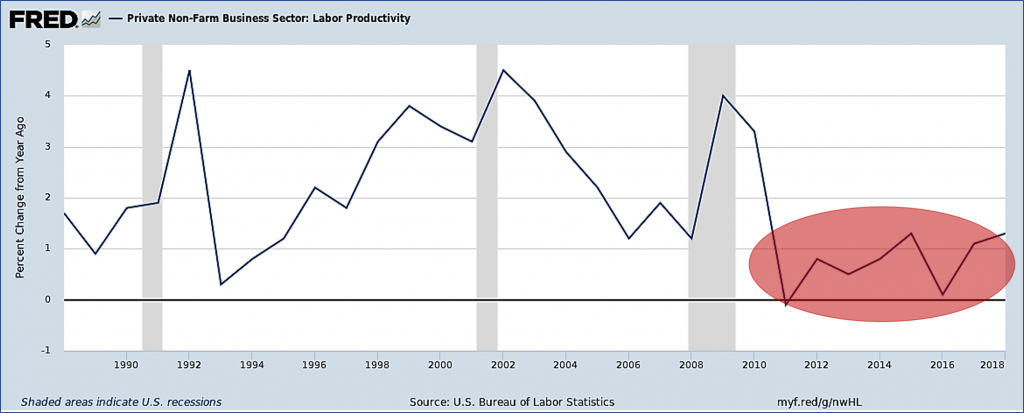

Let me explain. The value of money, like goods and services, is inversely tied to its demand and supply. For example, if the supply of bananas goes up relative to their demand, the price of bananas are likely to fall, and inversely if the supply falls relative to demand, the price will typically rise. So it is with money, if the supply of money rises relative to the demand for money, the price of money will typically fall and the effect of the CPI/M1, “the everyday” economy will be inflationary, meaning that money in relation to goods and services will become cheaper, or to explain a different way, the amount of money that you will need to purchase the same amount of goods, will be higher. So, what happens when the supply of money rises, but these inflationary effects aren’t seen in the day to day economy? There may be several reasons for this but I think in our situation, it indicates that the bullish borrowers, capitalists, businesses, and investors have left the pen of progress for the green pastures of easy earnings, and hence this “quantitative easing” that would usually cause inflationary pressures, isn’t circulating through the rest of the economy which would otherwise be evident in increased spending in business capital, rises in real wage rates etc. So, if this is the case, shouldn’t we see a slump in productivity growth despite the huge FED balance sheet growth? Yes. And we do:

Not only that but we see a similar story happening in Australia with the graph below showing the stagnation in business investment in Australia during the lead up to and after the GFC:

What’s interesting to note in this graph, is that non-mining capital expenditure is still below its 2008 high.

And, as long as business investment didn’t rise, CPI would not respond in proportion to QE. That is, while money can be created out of thin air through a process that’s easier than growing trees, economic growth is only created by individuals who have to assume risk in order to attain rewards, but, through the printing of endless cash, that beautiful risk and return relationship that grows a capitalist society (and arguably all economies), is destroyed.

From the very plan by central banks to save the global economy, we’ve experienced a complete economic zombification. Why? Well, take a read:

“Capitalist productivity, now 200+ years old, is becoming capitalist financialization.

What is financialization?

Financialization is profit margin growth without labor productivity growth.”

The reason companies aren’t investing more aggressively in plant and equipment and technology is BECAUSE we have the most accommodative monetary policy in the history of the world, with the easiest money to borrow that corporations have ever seen. Why in the world would management take the risk — and it’s definitely a risk — of investing for real growth when they are so awash in easy money that they can beat their earnings guidance with a risk-free stock buyback? Why in the world would management take the risk — and it’s definitely a risk — of investing for GAAP earnings when they are so awash in easy money that they can hit their pro forma narrative guidance by simply buying profitless revenue? Why in the world would companies take any risk at all when the Fed has eliminated any and all negative consequences for playing it safe? 7.

The reason postulated here for the lack of economic reinvestment is ultimately due to the culture of ease. Rather than creating a competitive dog-eat-dog business environment where the return is down the path of risk, prosperity, investment and courage, we’ve handed the candy to the corporates and made money cheap for the very organisations that once created wealth. Could it be that the very measures that central banks have taken to protect our private entities have ultimately gutted them to becoming lazy slobs? Could it be that this near ‘free money’ world has driven business to become as complacent as the ‘welfare bludgers’ that they so often criticize?

Guy Debelle, Deputy Governor of the RBA provides another narrative in relation to Australia’s business investment:

in reviewing possible explanations for why investment in the non-mining sector in Australia has been weak, the most powerful reason boils down to firms’ expectations of future demand, otherwise known as animal spirits. Mining investment was strong because expectations for future demand were high and there wasn’t that much uncertainty around that expectation. Expectations of demand elsewhere have not been strong. 8

This statement is so true that it almost doesn’t need to be said, so much so that it is self-evident to the problem, that is, if businesses thought wealth to be at the end of vast risk and investment, they would be doing so. The question is: why are the animal spirits awakened? And the answer, in this case, is in part, because central bankers have put the bulls of the business world to sleep with easy money. If quantitative easing along with expansionary monetary policies weren’t provided during the GFC, the pain would have been immense, no one would argue against that but, the endless injection of near-zero interest rates alongside QE 1, 2 & 3 have meant that the bullish business investments both in capital and labor that everyone was hoping for post GFC times, never came. Instead, we have had the biggest stock buyback period, ever with fewer reasons than ever before to be bullish on stocks.

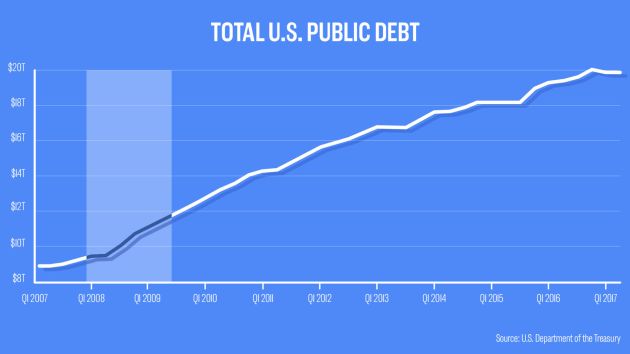

The problem with printing more money or lowering the cost of borrowing is that credit and cash have to go somewhere. In the states, it flooded into stocks as companies attempted to raise their profitability. In Australia and Canada, it flooded into housing driving up housing prices in major cities well beyond reasonable market PE ratios and as a result, inflating the short-term economic numbers. And while this cheap cash distorted the private sector and financialised the capitalist world, it also played havoc with Government bank accounts too with the US public debt now soaring well over $21 Trillion.

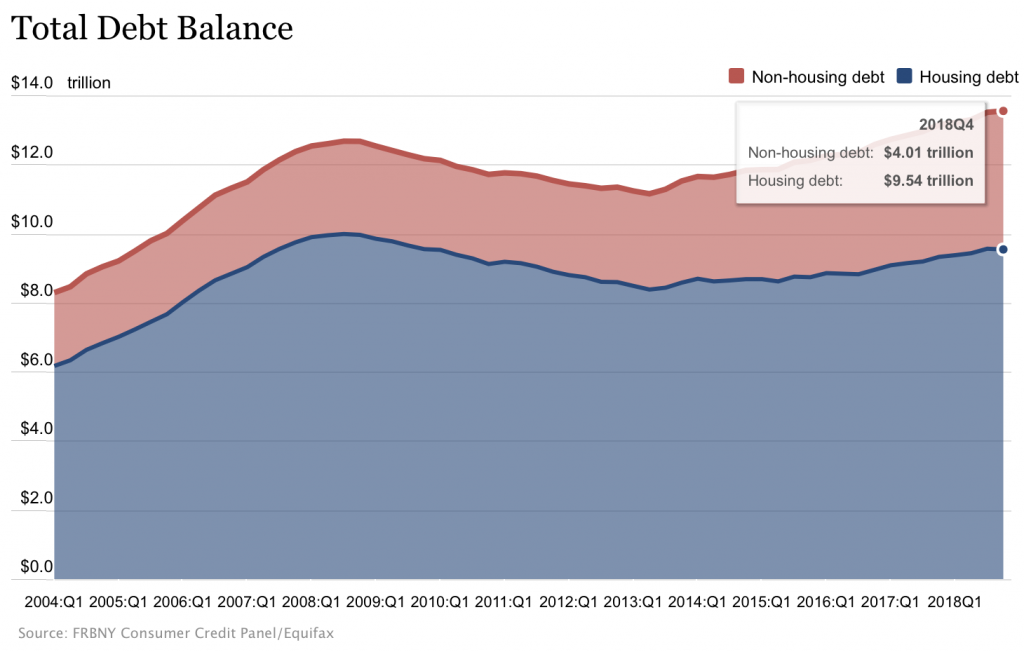

And while real wages and economic productivity have largely stalled, consumer debt hasn’t missed out on the party either with private individual debt now well above the disastrously high levels of 2008.

So here we are.

Welcome to the land of low business investment, low inflation, cheap and abundant cash, with low growth. And yes, this time it is made in America… and yes this time, it is a Japanese knock-off.

So why oh why is the FED alongside central governments globally playing this disastrous Keynesian game? Honestly, it’s because they’re afraid of the short term pain that normal interest rates would bring. They’re afraid of afflicting a depression that would likely follow after they stop the QE/low-interest-rate process. They’re so afraid in fact that they’ll bring out QE 4, 5 and 6! oh and 7, 8 and 9… they’re so afraid that they’re likely to continue printing money, inflating debt bubbles and shooting a dying economy with adrenaline, rather than face the music. The central bankers and Governments globally, are logical, but myopic. They’re no greater than the mobs that are tasked to govern, and because of this, we receive the policies that created the GFC and we receive the endless stimulus that’ll keep this debt glut going until it literally can’t anymore. Sometimes, the role of the government isn’t to deliver what the people want in the short term, sometimes the role of the government is to induce short term sacrifice for long term gain. Surely the mark of a society’s longevity isn’t its current economic state, but rather its concern for its future generations. When we personally borrow money, we increase short term consumption and decrease future consumption. When a state, a nation, an EU or a world, increase debt so significantly that it will take generations and generations to pay it off, they effectively increase short term consumption (in the form of consumerism, housing, schooling, medicine, military) at the expense of future generations consumption as ‘a benevolent person leaves an inheritance for his grandchildren’ 9, a society of unrestrained myopic hedonists will consume at the expense of their grandchildren. Both sides of the political fence are 100% guilty of propagating this generational theft. While the politicians, borrowers and business world have been complicit in creating this financial catastrophe, the previous administrations have been gutless in dealing with it. They’ve financialised the failures of the corrupt, robbed from the future, and passed on the reckless gambles to the greedy to the burden of the taxpayers and ultimately the financially disciplined savers. They’ve committed the greatest robbery the world has ever seen, yet for the time being, they’ve got away with it. Ultimately this will fall apart, the bill will come due and the world’s economy won’t survive.

There is a fundamental problem with the global economy that no president, no socialist program, no government and no reassuring words from the FED’s chairperson, can now fix. Neither will any economic shamanism, wizardry, genius, monetary policy or scholar conquer. Our only hope to fix this fundamental economic malaise can’t be found in the nominal world of numbers and policy, our only hope is in the fundamental. We need a fundamental miracle.

References:

- Niall Ferguson, The Ascent of Money A Financial History of the World. pg 158.(2008-2009).

- Niall Ferguson, The Ascent of Money A Financial History of the World. pg 159.(2008-2009).

- John Kenneth Galbraith, The Great Crash 1929. pg 146 (1954)

- Hebrews 12, NET Bible® copyright ©1996-2006 by Biblical Studies Press

- 1 Corinthians 15, New International Version®, NIV® Copyright ©1973, 1978, 1984, 2011

- Adam Smith, Wealth of Nations.

- Dr Ben Hunt, This is Water (2019), https://www.epsilontheory.com/this-is-water/ Accessed 1/06/2019

- Guy Debelle, Business Investment in Australia (November 2017) https://www.rba.gov.au/speeches/2017/sp-dg-2017-11-13.html

- Proverbs 13:22, NET Bible® copyright ©1996-2006 by Biblical Studies Press